Set Up Your LTD Company the Easy Way

Register your limited company online in minutes. Everything you need — in one place — done for you.

+200 000

Entrepreneurs

Rated Excellent

Companies House

Authorised Service Provider

100%

Satisfaction guaranteed

Trusted by Thousands of Business Owners

Same-day Set Up

I set up my company in less than a day. Super clear, super fast.

James K., Manchester

6 Feb 2024

Easy from the start

OnlineFilings made everything easy. Great value and excellent support.

Anita M., Bristol

12 Feb 2025

Easy from Abroad

As a non-resident, I appreciated how smooth it was. Highly recommended.

Omar D., Dubai

19 Jan 2024

Great for First-Time

First time starting a business. OnlineFilings made everything simple and stress-free.

Sarah M., Bristol

7 Jan 2025

Clear & Affordable

Registration was clear, fast, and much cheaper than going through an accountant.

Sophie N., London

27 Apr 2023

Same-day Set Up

I set up my company in less than a day. Super clear, super fast.

James K., Manchester

6 Feb 2024

Easy from the start

OnlineFilings made everything easy. Great value and excellent support.

Anita M., Bristol

12 Feb 2025

Easy from Abroad

As a non-resident, I appreciated how smooth it was. Highly recommended.

Omar D., Dubai

19 Jan 2024

Great for First-Time

First time starting a business. OnlineFilings made everything simple and stress-free.

Sarah M., Bristol

7 Jan 2025

Clear & Affordable

Registration was clear, fast, and much cheaper than going through an accountant.

Sophie N., London

27 Apr 2023

Same-day Set Up

I set up my company in less than a day. Super clear, super fast.

James K., Manchester

6 Feb 2024

Easy from the start

OnlineFilings made everything easy. Great value and excellent support.

Anita M., Bristol

12 Feb 2025

Easy from Abroad

As a non-resident, I appreciated how smooth it was. Highly recommended.

Omar D., Dubai

19 Jan 2024

Great for First-Time

First time starting a business. OnlineFilings made everything simple and stress-free.

Sarah M., Bristol

7 Jan 2025

Clear & Affordable

Registration was clear, fast, and much cheaper than going through an accountant.

Sophie N., London

27 Apr 2023

Same-day Set Up

I set up my company in less than a day. Super clear, super fast.

James K., Manchester

6 Feb 2024

Easy from the start

OnlineFilings made everything easy. Great value and excellent support.

Anita M., Bristol

12 Feb 2025

Easy from Abroad

As a non-resident, I appreciated how smooth it was. Highly recommended.

Omar D., Dubai

19 Jan 2024

Great for First-Time

First time starting a business. OnlineFilings made everything simple and stress-free.

Sarah M., Bristol

7 Jan 2025

Clear & Affordable

Registration was clear, fast, and much cheaper than going through an accountant.

Sophie N., London

27 Apr 2023

Everything in One Place

Company setup, VAT, and PAYE all handled through one platform. Brilliant service.

Lina G., Glasgow

16 Jul 2023

Fast & Friendly

Support team was responsive and friendly. Got my company number in 1 day.

Oliver M., Birmingham

23 Feb 2024

No Paperwork Needed

No paperwork, no jargon. Company formed online without hassle.

Rebecca S., Leeds

11 Nov 2023

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Everything in One Place

Company setup, VAT, and PAYE all handled through one platform. Brilliant service.

Lina G., Glasgow

16 Jul 2023

Fast & Friendly

Support team was responsive and friendly. Got my company number in 1 day.

Oliver M., Birmingham

23 Feb 2024

No Paperwork Needed

No paperwork, no jargon. Company formed online without hassle.

Rebecca S., Leeds

11 Nov 2023

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Everything in One Place

Company setup, VAT, and PAYE all handled through one platform. Brilliant service.

Lina G., Glasgow

16 Jul 2023

Fast & Friendly

Support team was responsive and friendly. Got my company number in 1 day.

Oliver M., Birmingham

23 Feb 2024

No Paperwork Needed

No paperwork, no jargon. Company formed online without hassle.

Rebecca S., Leeds

11 Nov 2023

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Everything in One Place

Company setup, VAT, and PAYE all handled through one platform. Brilliant service.

Lina G., Glasgow

16 Jul 2023

Fast & Friendly

Support team was responsive and friendly. Got my company number in 1 day.

Oliver M., Birmingham

23 Feb 2024

No Paperwork Needed

No paperwork, no jargon. Company formed online without hassle.

Rebecca S., Leeds

11 Nov 2023

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Overseas Set Up

Formed my UK company from abroad. Fast turnaround and clear guidance.

Sergio H., Madrid

3 Jan 2024

Our simple 4-Step company formation process

Step 1

Choose a Company Name

Step 2

Select Your Package

Step 3

Checkout Securely

Step 4

Complete Your Order

Why register your company with Online Filings?

Fast & Easy

Set up your limited company online in just minutes; most applications are approved within 3 business hours.

Expert Support

Get personal, unhurried lifetime help from our company formation experts by phone, email or chat.

Protect Your Privacy

Use our registered office address to keep your home address off public records and give your company a professional image.

Protect your privacy with our london address services

Frequently Asked Questions about Setting up an LTD company

Everything you need to know about incorporating a company

Can’t find an answer?

Most companies are registered within 3 to 6 working hours, and often even faster. It depends on Companies House processing times, but our fast company registration process ensures we submit your application immediately and without delays.

To set up your LTD company, you’ll need:

- A company name (check availability with our search tool)

- A registered office address in the UK

- Details for at least one director and one shareholder

- A service address for each director

- Share allocation details

- We’ll guide you through each step — no guesswork required

Yes. You can be the sole director and sole shareholder of your limited company. Many small businesses start this way — it’s perfectly legal and very common.

You don’t need an accountant to register your company. However, once your business is running, an accountant can help you manage tax returns, annual accounts, and VAT. We also offer tools and partners to support you after formation if needed.

Every UK company must file:

- A Confirmation Statement - once a year

- Annual Accounts (even if the company is dormant) Other potential filings include Corporation Tax and PAYE. You can manage these yourself or use our services to stay compliant with Companies House and HMRC.

The main difference is liability. As a sole trader, you're personally responsible for business debts. With a limited company, your business is a separate legal entity — which means your personal assets are protected. Limited companies also look more professional and may offer better tax efficiency.

Yes, but your address will appear on the public Companies House register unless you use a registered office address and service address (UK). That’s why many entrepreneurs choose our business address service — to work from anywhere without exposing their home details.

Yes, unless you use an address service. When you register a company, Companies House publishes your registered and director addresses online. To protect your privacy, we offer a London registered office and virtual mailbox so your personal details stay private and secure.

Identity verification is a requirement introduced by the Economic Crime and Corporate Transparency Act 2023. Companies House is moving to a system where all company directors must verify their identity, and this requirement applies to filings submitted through Online Filings.

Online Filings is an Authorised Corporate Service Provider (ACSP) registered with Companies House and is supervised by HMRC for Anti-Money Laundering. Because of these obligations, we must verify the identity of all directors and all users before any filing can be submitted through our platform. This protects the integrity of the service and ensures that every filing we process is valid and compliant with UK law.

Directors using Online Filings must therefore complete identity verification before we can submit their filing. The process is fast, secure and takes less than two minutes on your smartphone. You can verify your identity using a UK driving licence, a UK passport or an international passport.

The Companies House Personal Code is an 11-character identifier you receive after completing identity verification with Companies House. From 18 November 2025, all directors, people with significant control (PSCs) and other key company officers must use this code when submitting filings such as confirmation statements and appointment forms.

You only need to verify your identity once. Your personal code will then apply to all your current and future roles and appointments. Keep your code secure, but you may share it with trusted professionals such as accountants, authorised agents or the Online Filings platform when they submit filings on your behalf.

When do I need to use my Personal Code?

- Directors: Use the code when filing the company's confirmation statement or when being appointed.

- PSCs who are not directors: Provide your code within 14 days of the start of your birth month.

Online Filings is officially approved by Companies House as an Authorised Corporate Service Provider. This status means we are trusted to submit your company filings directly to Companies House on your behalf, following rigorous compliance and security standards required by UK law.

As an ACSP, we must:

- Verify the identity of directors and people with significant control (PSCs) using government-approved processes.

- Follow strict anti-money laundering checks overseen by Companies House and a UK supervisory body such as HMRC.

- Protect your company from fraud and ensure your filings are always accurate, secure, and fully compliant with UK regulations.

Using Online Filings means your documents are managed by a government-recognised and highly regulated provider, giving you a smoother, safer, and more reliable experience.

Can’t find an answer?

Start, Manage & Grow Your Business – All in One

Identity Verification made simple with Online Filings

All company directors must now verify their identity with Companies House. Online Filings makes this fast and simple.

You can request your 11-character Companies House Personal Code directly from your Online Filings dashboard. To verify your identity, just take a photo of your UK driving licence, UK passport or international passport, and then take a few quick face snapshots to match your document with your mobile or webcam.

The process takes about 80 seconds and keeps your company fully compliant. All identity data is processed in full compliance with UK GDPR.

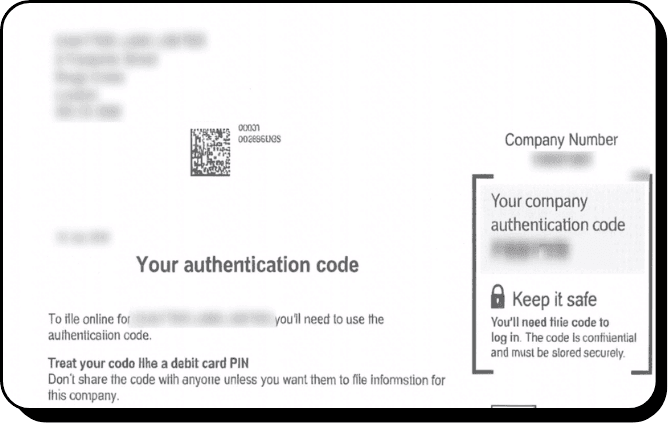

Your authentication code authorises your filing

Your Companies House Authentication Code is your company's secure digital signature. It is a six-character alphanumerical code that was sent to you when you incorporated your business. Companies House will not accept any filing without it, and no service provider can submit on your behalf unless you provide this code.

Lost your code? You can request Companies House to resend the code on file to your registered office address in just one click from your Online Filings dashboard. For security, the code is sent only by letter and usually arrives within 10 working days.

Ready to set up your LTD company today?

Register your limited company quickly and easily with a trusted platform that handles everything — from setup to support.

Register Your Company

Prefer to speak with someone?

Call 020 4538 3610

or email us at support@onlinefilings.co.uk