Register for PAYE with HMRC in Just a Few Clicks

Set up your PAYE scheme online with Online Filings and get your HMRC employer reference number without the paperwork. Fast, compliant, and built for limited companies and small employers.

Find your company to start your PAYE Registration:

+200 000

Entrepreneurs

Rated Excellent

Companies House

Authorised Service Provider

100%

Satisfaction guaranteed

Trusted by thousands of new employers across the UK

Super simple

PAYE felt complex, but they made it incredibly simple. Great experience!

Ben C., Bristol

9 Jan 2024

Perfect for directors

Needed PAYE to pay myself. OnlineFilings made it quick, simple, and stress-free.

Simran T., Croydon

10 Jan 2024

Quick & Efficient

Form took minutes. Got my PAYE references from HMRC fast and without any issues.

Fatima K., Reading

2 Mar 2023

Stress-Free Filing

I worry about admin, but this was easy. PAYE registration felt totally manageable.

Mark S., Glasgow

19 Nov 2023

Great for Startups

Registered my PAYE as a new director. Fast, helpful, and fully online.

Tom S., Cardiff

22 Apr 2024

Super simple

PAYE felt complex, but they made it incredibly simple. Great experience!

Ben C., Bristol

9 Jan 2024

Perfect for directors

Needed PAYE to pay myself. OnlineFilings made it quick, simple, and stress-free.

Simran T., Croydon

10 Jan 2024

Quick & Efficient

Form took minutes. Got my PAYE references from HMRC fast and without any issues.

Fatima K., Reading

2 Mar 2023

Stress-Free Filing

I worry about admin, but this was easy. PAYE registration felt totally manageable.

Mark S., Glasgow

19 Nov 2023

Great for Startups

Registered my PAYE as a new director. Fast, helpful, and fully online.

Tom S., Cardiff

22 Apr 2024

Super simple

PAYE felt complex, but they made it incredibly simple. Great experience!

Ben C., Bristol

9 Jan 2024

Perfect for directors

Needed PAYE to pay myself. OnlineFilings made it quick, simple, and stress-free.

Simran T., Croydon

10 Jan 2024

Quick & Efficient

Form took minutes. Got my PAYE references from HMRC fast and without any issues.

Fatima K., Reading

2 Mar 2023

Stress-Free Filing

I worry about admin, but this was easy. PAYE registration felt totally manageable.

Mark S., Glasgow

19 Nov 2023

Great for Startups

Registered my PAYE as a new director. Fast, helpful, and fully online.

Tom S., Cardiff

22 Apr 2024

Super simple

PAYE felt complex, but they made it incredibly simple. Great experience!

Ben C., Bristol

9 Jan 2024

Perfect for directors

Needed PAYE to pay myself. OnlineFilings made it quick, simple, and stress-free.

Simran T., Croydon

10 Jan 2024

Quick & Efficient

Form took minutes. Got my PAYE references from HMRC fast and without any issues.

Fatima K., Reading

2 Mar 2023

Stress-Free Filing

I worry about admin, but this was easy. PAYE registration felt totally manageable.

Mark S., Glasgow

19 Nov 2023

Great for Startups

Registered my PAYE as a new director. Fast, helpful, and fully online.

Tom S., Cardiff

22 Apr 2024

No Delays, Just Done

Hired our first team. They registered PAYE fast and we were compliant right away.

George M., Brighton

6 Sep 2023

So worth it

Skipped the DIY stress. OnlineFilings did it all, with no confusion or delays.

Tomas J., Birmingham

16 Dec 2023

Seamless Setup

Set up my company and came back for PAYE. Seamless, smooth and solo-founder friendly.

Jordan R., Bristol

22 Jan 2024

Perfect for agencies

Registered PAYE for our first employee. Clear, quick and no confusion at all.

Ella K., Cambridge

9 Nov 2023

Great service twice

Used them for VAT and PAYE. Both were fast and flawless experiences.

Ben T., Glasgow

7 Mar 2024

No Delays, Just Done

Hired our first team. They registered PAYE fast and we were compliant right away.

George M., Brighton

6 Sep 2023

So worth it

Skipped the DIY stress. OnlineFilings did it all, with no confusion or delays.

Tomas J., Birmingham

16 Dec 2023

Seamless Setup

Set up my company and came back for PAYE. Seamless, smooth and solo-founder friendly.

Jordan R., Bristol

22 Jan 2024

Perfect for agencies

Registered PAYE for our first employee. Clear, quick and no confusion at all.

Ella K., Cambridge

9 Nov 2023

Great service twice

Used them for VAT and PAYE. Both were fast and flawless experiences.

Ben T., Glasgow

7 Mar 2024

No Delays, Just Done

Hired our first team. They registered PAYE fast and we were compliant right away.

George M., Brighton

6 Sep 2023

So worth it

Skipped the DIY stress. OnlineFilings did it all, with no confusion or delays.

Tomas J., Birmingham

16 Dec 2023

Seamless Setup

Set up my company and came back for PAYE. Seamless, smooth and solo-founder friendly.

Jordan R., Bristol

22 Jan 2024

Perfect for agencies

Registered PAYE for our first employee. Clear, quick and no confusion at all.

Ella K., Cambridge

9 Nov 2023

Great service twice

Used them for VAT and PAYE. Both were fast and flawless experiences.

Ben T., Glasgow

7 Mar 2024

No Delays, Just Done

Hired our first team. They registered PAYE fast and we were compliant right away.

George M., Brighton

6 Sep 2023

So worth it

Skipped the DIY stress. OnlineFilings did it all, with no confusion or delays.

Tomas J., Birmingham

16 Dec 2023

Seamless Setup

Set up my company and came back for PAYE. Seamless, smooth and solo-founder friendly.

Jordan R., Bristol

22 Jan 2024

Perfect for agencies

Registered PAYE for our first employee. Clear, quick and no confusion at all.

Ella K., Cambridge

9 Nov 2023

Great service twice

Used them for VAT and PAYE. Both were fast and flawless experiences.

Ben T., Glasgow

7 Mar 2024

How to register your business for PAYE? 4 easy steps

Step 1

Search Your Company and Get Started

Step 2

Provide Business and Start Date Details

Step 3

Authenticate and Verify in Minutes

Step 4

We File with HMRC and You Receive Your PAYE Reference

Get Started with PAYE Registration

Why choose Online Filings for your PAYE registration?

Effortless, Jargon-Free Experience

Our smart, mobile-friendly forms are short and clear. With a direct link to Companies House, we auto-fill your company details so you can register for PAYE quickly and easily.

We Handle the Paperwork (Even When You’ve Lost It)

Missing your Companies House authentication code or Corporation Tax UTR? No problem. With just one click, we request them securely by post to your registered office. You don’t need to dig through old files or chase government forms.

Real Human Support and HMRC-Free Filing

We’ve helped hundreds of UK businesses complete their PAYE registration. Our expert team is available by email, phone, or chat. No more waiting on hold with HMRC. With secure ID and biometric checks, you can file quickly and compliantly from your smartphone.

PAYE registration FAQs

Everything you need to know about PAYE registration

Can’t find an answer?

PAYE (Pay As You Earn) is the system used by HMRC to collect income tax and National Insurance from employees’ wages. If you're planning to hire staff or pay yourself a salary through your limited company, you must register for PAYE with HMRC.

You can register directly with HMRC or use Online Filings to handle the process for you. Our online PAYE registration service is quick, compliant, and avoids the complexity of government forms.

Yes. Our service is ideal for limited company PAYE registration. We help you set up a PAYE scheme and ensure everything is submitted correctly to HMRC.

A PAYE scheme is required if you plan to pay any employees or yourself £96 or more per week (for the 2025/26 tax year). It’s mandatory for most businesses that employ staff and for limited company directors who pay themselves a salary at or above this threshold. We handle the full PAYE scheme registration on your behalf to ensure compliance with HMRC regulations.

You’ll need your company’s details (including the Companies House number), your Corporation Tax UTR, director details, and the date you plan to start paying staff. We simplify this process by pre-filling available information where possible.

HMRC typically takes 5 to 15 working days to process the PAYE registration. We submit your application instantly and follow up if they request additional information.

Yes. Our platform supports employer PAYE registration online, whether you're a sole director or hiring employees. Everything is done digitally with real support if you need help.

If you want to pay yourself a salary through your company, you still need to register as an employer. Even one-person limited companies often require PAYE registration to stay compliant.

Yes. If HMRC requests further details or documents, we deal with them directly to save you the hassle.

Identity verification is a requirement introduced by the Economic Crime and Corporate Transparency Act 2023. Companies House is moving to a system where all company directors must verify their identity, and this requirement applies to filings submitted through Online Filings.

Online Filings is an Authorised Corporate Service Provider (ACSP) registered with Companies House and is supervised by HMRC for Anti-Money Laundering. Because of these obligations, we must verify the identity of all directors and all users before any filing can be submitted through our platform. This protects the integrity of the service and ensures that every filing we process is valid and compliant with UK law.

Directors using Online Filings must therefore complete identity verification before we can submit their filing. The process is fast, secure and takes less than two minutes on your smartphone. You can verify your identity using a UK driving licence, a UK passport or an international passport.

Online Filings is officially approved by Companies House as an Authorised Corporate Service Provider. This status means we are trusted to submit your company filings directly to Companies House on your behalf, following rigorous compliance and security standards required by UK law.

As an ACSP, we must:

- Verify the identity of directors and people with significant control (PSCs) using government-approved processes.

- Follow strict anti-money laundering checks overseen by Companies House and a UK supervisory body such as HMRC.

- Protect your company from fraud and ensure your filings are always accurate, secure, and fully compliant with UK regulations.

Using Online Filings means your documents are managed by a government-recognised and highly regulated provider, giving you a smoother, safer, and more reliable experience.

Can’t find an answer?

Register as an employer with an HMRC recognised provider

Identity Verification made simple with Online Filings

All company directors must now verify their identity with Companies House. Online Filings makes this fast and simple.

You can request your 11-character Companies House Personal Code directly from your Online Filings dashboard. To verify your identity, just take a photo of your UK driving licence, UK passport or international passport, and then take a few quick face snapshots to match your document with your mobile or webcam.

The process takes about 80 seconds and keeps your company fully compliant. All identity data is processed in full compliance with UK GDPR.

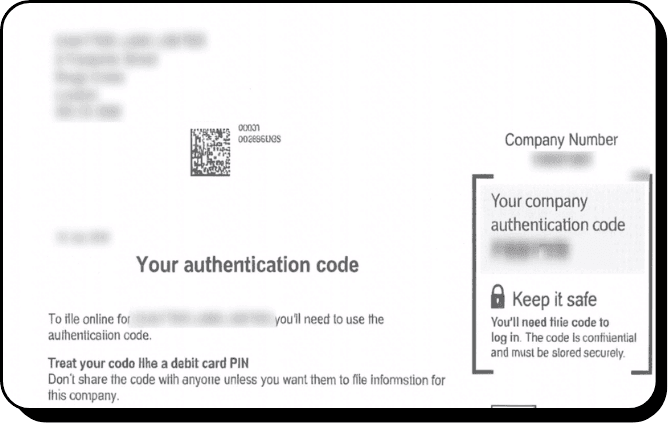

Your authentication code authorises your filing

Your Companies House Authentication Code is your company's secure digital signature. It is a six-character alphanumerical code that was sent to you when you incorporated your business. Companies House will not accept any filing without it, and no service provider can submit on your behalf unless you provide this code.

Lost your code? You can request Companies House to resend the code on file to your registered office address in just one click from your Online Filings dashboard. For security, the code is sent only by letter and usually arrives within 10 working days.

Ready to register your business for PAYE?

Register for PAYE

Prefer to speak with someone?

Call 020 4538 3610

or email us at support@onlinefilings.co.uk